Behavioral Finance: Understanding How Emotions Affect Your Money Decisions

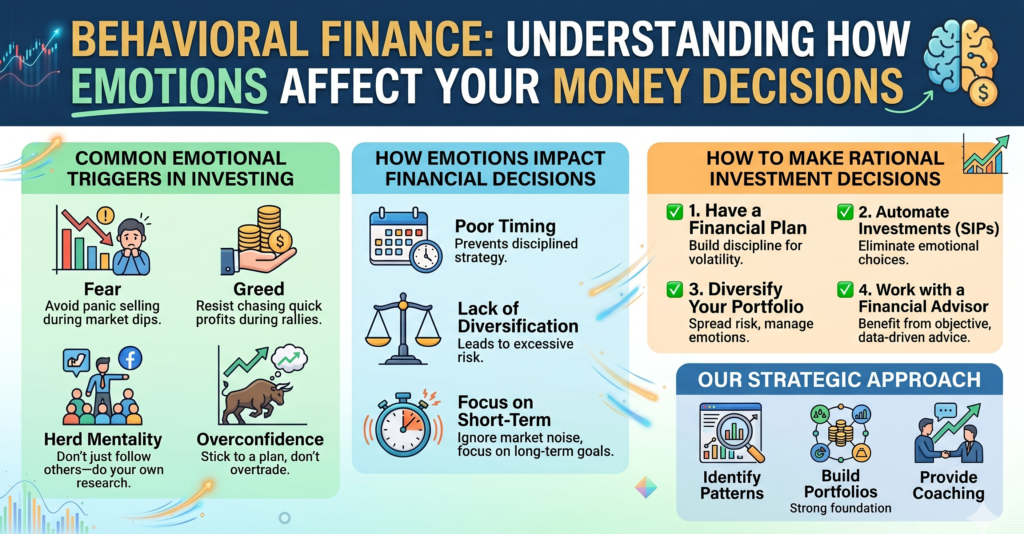

When it comes to money, logic often takes a back seat. Our emotions—fear, greed, excitement, and anxiety—play a big role in how we invest, spend, and save. This intersection of psychology and finance is called Behavioral Finance.

At Dhingra Wealth, we help investors understand how emotions impact financial decisions and guide them to make rational, data-driven choices for long-term success.

What is Behavioral Finance?

Behavioral finance studies how human emotions and cognitive biases influence financial behavior.

Even the most experienced investors are not immune to emotional decision-making—buying high in excitement or selling low in panic.

The goal of understanding behavioral finance is to recognize these biases and learn how to control them.

Common Emotional Triggers in Investing

- Fear

When markets fall, fear makes investors sell in panic—often locking in losses instead of waiting for recovery.

- Greed

During bull runs, greed pushes investors to chase quick profits, ignoring fundamentals or risk.

- Overconfidence

Thinking we “know the market” can lead to excessive trading and risk-taking.

- Herd Mentality

Following others—friends, family, or social media trends—without personal research can derail financial goals.

- Loss Aversion

People feel the pain of losing money twice as much as the joy of gaining it, which often leads to poor timing decisions.

How Emotions Impact Financial Decisions

- Buying high and selling low instead of following a disciplined investment strategy

- Ignoring diversification out of fear or greed

- Reacting to short-term market noise instead of focusing on long-term goals

- Avoiding investments altogether due to fear of loss

How to Make Rational Investment Decisions

1. Have a Financial Plan

1. Have a Financial Plan

A clear plan aligned with your goals helps you stay disciplined even during market volatility.

2. Automate Investments

Systematic Investment Plans (SIPs) eliminate emotional decision-making by investing regularly.

3. Avoid Constant Market Monitoring

Checking your portfolio daily increases anxiety. Long-term investing works best with patience.

4. Diversify Your Portfolio

Spread investments across asset classes to reduce risk and emotional swings.

5. Work with a Financial Advisor

A professional like Dhingra Wealth brings objectivity and helps you make decisions based on data, not emotion.

Dhingra Wealth’s Approach

At Dhingra Wealth, we combine financial planning with behavioral awareness. We help clients:

- Identify emotional patterns that affect money decisions

- Build portfolios designed to reduce reactionary behavior

- Provide coaching to stay disciplined through market ups and downs

Conclusion

Your emotions can be your biggest enemy—or your greatest ally—when it comes to investing.

Understanding behavioral finance helps you recognize biases and make smarter, calmer decisions.

Let Dhingra Wealth guide you toward a more balanced, emotion-free approach to wealth creation.

Let Dhingra Wealth guide you toward a more balanced, emotion-free approach to wealth creation.

Common Cognitive Biases That Lead to Bad Investment Choices

Even smart investors make poor financial decisions—not because they lack knowledge, but because of hidden mental shortcuts called cognitive biases. These biases shape how we think about money, risk, and reward, often leading us away from rational investing.

At Dhingra Wealth, we help investors identify and overcome these biases so they can make clear, objective, and goal-focused decisions.

What Are Cognitive Biases?

Cognitive biases are psychological patterns that cause us to make decisions based on emotions, perceptions, or habits rather than facts and logic.

In investing, these biases can cloud judgment, making us buy, sell, or hold at the wrong time.

Top Cognitive Biases That Affect Investors

1. Confirmation Bias

1. Confirmation Bias

Investors seek information that supports their existing beliefs and ignore data that contradicts them.

Example: Believing a certain stock will perform well and only reading positive news about it.

How to Avoid:

Look for both pros and cons before making a decision. Rely on data, not opinions.

2. Overconfidence Bias

2. Overconfidence Bias

Many investors believe they can “beat the market” based on intuition or short-term success.

Example: Trading frequently without a clear strategy, assuming every pick will succeed.

How to Avoid:

Stick to your investment plan and recognize that no one predicts the market consistently.

3. Herd Mentality

3. Herd Mentality

Following what everyone else is doing—whether it’s buying trending stocks or selling during panic.

Example: Investing because “everyone is investing in it,” without understanding fundamentals.

How to Avoid:

Base decisions on your own financial goals and risk appetite, not crowd behavior.

4. Loss Aversion Bias

4. Loss Aversion Bias

The fear of losing money makes investors hold on to poor investments or sell winners too early.

Example: Refusing to sell a falling stock in the hope it will recover soon.

How to Avoid:

Focus on long-term portfolio performance, not short-term losses.

5. Anchoring Bias

5. Anchoring Bias

Fixating on a reference point (like an old price) when making financial decisions.

Example: Refusing to sell a stock until it “gets back to the price I bought it.”

How to Avoid:

Reassess investments based on current potential, not past prices.

6. Recency Bias

6. Recency Bias

Placing too much importance on recent events rather than long-term trends.

Example: Investing more in an asset because it performed well last month.

How to Avoid:

Evaluate performance over several years, not just recent market movements.

How These Biases Impact Your Wealth

- Poor timing decisions (buying high, selling low)

- Missed diversification opportunities

- Emotional investing instead of goal-based investing

- Overexposure to risk due to false confidence

How Dhingra Wealth Helps

We guide clients to make data-driven and emotion-free investment decisions by:

- Conducting regular portfolio reviews

- Educating clients on behavioral finance

- Using structured investment strategies like SIPs

- Aligning decisions with personal goals, not market noise

Conclusion

Cognitive biases are part of human nature—but recognizing them is the first step toward smarter investing.

By staying objective and disciplined, you can avoid emotional traps and grow your wealth steadily.

Partner with Dhingra Wealth to invest intelligently and overcome the biases that hold you back.

Why People Panic Sell — Lessons from Market Volatility

Market volatility can make even seasoned investors uneasy.

When markets fall sharply, panic often replaces patience — leading many to sell good investments at the worst possible time.

At Dhingra Wealth, we believe understanding the psychology behind panic selling is key to becoming a disciplined, long-term investor.

- The Emotional Rollercoaster of Investing

Investing isn’t just about numbers — it’s about emotions.

When markets rise, confidence and excitement take over.

When they fall, fear and uncertainty creep in.

This emotional cycle often leads to buying high and selling low — the exact opposite of what smart investing requires.

- What Is Panic Selling?

Panic selling happens when investors react emotionally to short-term market declines and sell off investments to “cut losses.”

But in doing so, they often lock in losses that could have been temporary on paper.

Example:

During the COVID-19 crash of 2020, markets fell over 35% in a month — but recovered within the same year.

Investors who sold in fear missed the rebound.

- Why Do Investors Panic Sell?

a. Loss Aversion

The pain of losing money is psychologically twice as strong as the joy of gaining it.

b. Herd Behavior

When everyone is selling, investors feel safer following the crowd — even if it means acting irrationally.

c. Media Noise

c. Media Noise

Constant headlines about “market crashes” amplify fear and make investors overreact.

d. Short-Term Focus

d. Short-Term Focus

Instead of focusing on long-term goals, investors fixate on daily portfolio fluctuations.

- What Happens When You Sell in Panic

- You realize permanent losses that may have been temporary

- You miss the market rebound

- You disrupt your financial plan

- You lose the power of compounding that works best during recovery phases

Remember: Every crash in history has eventually been followed by a recovery.

- How to Avoid Panic Selling

Stick to Your Financial Plan

Your plan is designed for the long term — not daily market movements.

Diversify Your Portfolio

Diversify Your Portfolio

A well-diversified portfolio cushions volatility and reduces emotional reactions.

Detach Emotionally

Detach Emotionally

Treat investing like a disciplined routine, not a day-to-day performance test.

Focus on Time in the Market

Focus on Time in the Market

History shows — staying invested through volatility leads to better outcomes than timing the market.

- The Dhingra Wealth Approach

At Dhingra Wealth, we help investors:

- Stay focused on long-term financial goals

- Conduct regular reviews to ensure portfolio health

- Understand market psychology and not react impulsively

- Build emergency funds so short-term needs don’t force hasty decisions

Our approach helps clients stay invested, stay calm, and stay confident — even during market storms.

- Key Takeaway

Volatility is not your enemy — emotion is.

The best investors aren’t those who avoid market drops but those who manage their reactions to them.

Stay disciplined. Stay patient.

Because in the long run, time rewards the calm investor.

Cybersecurity and Financial Risk — Protecting Your Digital Assets

In today’s digital world, your financial life is no longer confined to bank lockers and paper documents — it lives online.

From internet banking to investment apps and digital wallets, convenience has brought along a new kind of risk — cyber risk.

At Dhingra Wealth, we believe protecting your digital assets is now as essential as protecting your physical wealth.

- The Digital Shift in Personal Finance

Most of us manage almost everything online — investing, paying bills, filing taxes, or tracking expenses.

While this digital shift has made life easier, it has also opened doors for cyber threats such as data breaches, identity theft, and financial fraud.

A single weak password or an unverified link can put your entire financial profile at risk.

- What Are Digital Financial Assets?

Digital assets include:

- Online bank accounts and investment platforms

- Mutual fund and insurance portals

- Trading accounts and demat holdings

- Cryptocurrencies and digital wallets

- Sensitive personal and financial data stored online

Losing access to these or having them compromised can cause serious financial damage.

- Common Cyber Threats Targeting Investors

Phishing Scams

Phishing Scams

Fake emails or messages tricking you into sharing login credentials or OTPs.

Malware & Ransomware

Malware & Ransomware

Software designed to steal or block access to your financial data.

Fraudulent Apps

Fraudulent Apps

Unverified apps posing as legitimate financial services.

Social Engineering

Social Engineering

Hackers manipulating people into revealing confidential information.

- The Financial Impact of a Cyber Breach

Cyber fraud doesn’t just lead to monetary loss — it disrupts your trust in financial systems, causes emotional stress, and may affect your credit score and long-term financial goals.

- How to Protect Your Digital Wealth

a. Use Strong, Unique Passwords

a. Use Strong, Unique Passwords

Avoid reusing passwords across platforms. Consider a password manager for better security.

b. Enable Two-Factor Authentication

b. Enable Two-Factor Authentication

An extra layer of protection that ensures only you can access your accounts.

c. Beware of Suspicious Links

c. Beware of Suspicious Links

Never click links in unsolicited emails, messages, or calls claiming to be from your bank or broker.

d. Monitor Your Accounts Regularly

d. Monitor Your Accounts Regularly

Review bank and investment statements monthly to spot unusual transactions early.

e. Secure Your Devices

e. Secure Your Devices

Keep your phone and laptop updated, use antivirus software, and avoid public Wi-Fi for financial transactions.

- Cybersecurity and Financial Planning Go Hand in Hand

Cybersecurity is not just an IT concern — it’s a financial planning essential.

Protecting your data ensures your wealth-building efforts are not undone by a single incident.

At Dhingra Wealth, we help clients integrate digital safety into their overall wealth strategy, including:

- Secure document storage

- Verified investment platforms

- Education on cyber hygiene

- The Future of Financial Protection

As India moves toward a fully digital economy, digital risk insurance and cybersecurity tools are becoming critical components of financial wellbeing.

The future investor must protect not only where they invest but also how they invest.

- Key Takeaway

Your wealth deserves protection — both offline and online.

By adopting good digital habits and staying vigilant, you can ensure your financial future remains safe, smart, and secure.

Because in today’s world, financial literacy without cyber literacy is incomplete.

The Psychology of Risk — Why We Fear Loss More Than We Value Gains

Investing isn’t just about numbers and charts — it’s also about emotions.

At Dhingra Wealth, we often say: “Managing money begins with managing mindset.”

And one of the most powerful emotions that influences financial decisions is fear — specifically, the fear of losing money.

- Understanding the Concept of Loss Aversion

Psychologists Daniel Kahneman and Amos Tversky discovered a behavioral bias called loss aversion — the idea that losing ₹1 feels twice as painful as the pleasure of gaining ₹1.

This means investors are often more focused on avoiding losses than on pursuing gains — even when opportunities are sound.

Example:

If your investment falls 10%, you might panic and sell — but if it rises 10%, you’re only mildly pleased. That emotional imbalance can affect long-term wealth creation.

- How Fear Shapes Investment Decisions

When emotions drive decisions, logic takes a back seat.

Some common emotional reactions include:

- Selling too early when markets dip (to “protect capital”)

- Holding cash instead of investing (fear of making the wrong choice)

- Avoiding equity even when the goal is long-term growth

- Chasing trends after markets rally (fear of missing out)

These behaviors don’t eliminate risk — they shift it from market risk to missed opportunity risk.

- Why Our Brains Are Wired for Safety

Our ancestors survived by being alert to danger — that instinct still lives in us.

But while it helped avoid predators, it now makes us overly cautious in financial decisions.

Our brain perceives market volatility as “danger,” triggering anxiety — even though, in investing, volatility is often temporary.

- The Cost of Emotional Investing

Emotional investing often leads to:

- Poor timing — buying high and selling low

- Missed compounding — breaking SIPs too early

- Portfolio imbalance — avoiding riskier but necessary asset classes

Over time, these actions can cost investors more than any short-term market correction.

- Reframing How We See Risk

At Dhingra Wealth, we help clients redefine risk — not as something to avoid, but something to understand and manage.

Consider this mindset shift:

“Equity is risky.” “Equity volatility is temporary; inflation risk is permanent.”

“Equity is risky.” “Equity volatility is temporary; inflation risk is permanent.”

When you view risk as a tool, not a threat, you start making smarter long-term decisions.

- Strategies to Overcome Loss Aversion

a. Focus on Long-Term Goals

Markets move daily, but your goals are multi-year. Align your emotions with your time horizon.

b. Automate Your Investments

SIPs reduce emotional decision-making and bring discipline.

c. Diversify Smartly

A mix of equity, debt, and gold cushions volatility and builds confidence.

d. Review, Don’t React

d. Review, Don’t React

Periodic portfolio reviews ensure balance without emotional reactions.

- How Advisors Help Manage Behavioral Risk

A financial advisor acts as an emotional anchor.

At Dhingra Wealth, we guide clients through uncertain times by:

- Providing perspective during volatility

- Helping avoid impulsive exits

- Keeping financial plans aligned with goals, not emotions

- The Balance Between Logic and Emotion

Good investing doesn’t mean ignoring emotions — it means understanding them.

Fear and greed are part of being human. But by recognizing their influence, you can make more rational, confident decisions.

- Key Takeaway

You can’t remove risk from investing — but you can control how you respond to it.

By mastering your emotions, you gain the confidence to stay invested, ride out volatility, and truly benefit from compounding.

Because ultimately, your mind is your greatest investment tool.

Emotional Diversification — Balancing Heart and Mind in Investing

Investing is often seen as a purely logical process — numbers, charts, and returns dominate the discussion.

Yet, emotions play a significant role in financial decisions. Balancing heart and mind is essential for smart investing.

At Dhingra Wealth, we help clients achieve emotional diversification, ensuring that feelings like fear, greed, or impatience do not derail their long-term financial goals.

- What Is Emotional Diversification?

Emotional diversification is the practice of recognizing and managing the emotional factors that influence financial decisions.

Just as you diversify your portfolio across asset classes, you should diversify your emotions when making financial choices.

- Why Emotions Matter in Investing

Emotions can cause:

- Panic selling during market downturns

- Chasing trends after market rallies

- Avoiding necessary risks due to fear

- Overconfidence, leading to excessive trading

Even disciplined investors can fall prey to emotional decision-making if not mindful.

- Common Emotional Pitfalls

Fear

Fear

Fear of loss can make investors hold cash or sell at the wrong time.

Greed

Greed

Greed pushes people to chase high returns without assessing risk.

Impatience

Impatience

Wanting quick gains often leads to abandoning long-term strategies.

Herd Mentality

Herd Mentality

Following others blindly instead of making personal, goal-aligned choices.

- How to Achieve Emotional Diversification

1. Stick to a Financial Plan

A well-structured plan acts as an anchor during market volatility.

2. Automate Investments

SIPs and automated contributions reduce the chances of reactionary decisions.

3. Diversify Portfolio

A mix of equity, debt, gold, and liquid assets balances financial risk and emotional stress.

4. Educate Yourself

Understanding market cycles and investment principles reduces fear and impulsiveness.

5. Review, Don’t React

Periodic portfolio reviews allow adjustments without knee-jerk decisions.

- The Dhingra Wealth Approach

We help clients:

- Recognize behavioral patterns affecting financial decisions

- Implement goal-based investing strategies

- Build portfolios designed to withstand market volatility

- Balance emotions and rational decision-making

By guiding clients through both financial and emotional landscapes, we ensure smarter, calmer, and more disciplined investing.

- Key Takeaway

Investing successfully requires more than numbers — it demands emotional intelligence.

By practicing emotional diversification, you can reduce the impact of fear, greed, and impulsiveness, ensuring your portfolio stays aligned with your goals.

Remember: A well-managed mind is as important as a well-managed portfolio.

Wealth Protection — Why Risk Management is Part of Financial Planning

Building wealth is one part of financial success; protecting it is equally important.

Without proper risk management, unforeseen events like illness, accidents, or market downturns can derail years of careful planning.

At Dhingra Wealth, we believe risk management is not optional — it’s foundational to comprehensive financial planning.

- What Is Wealth Protection?

Wealth protection involves strategies that safeguard your assets from financial shocks, ensuring that your savings, investments, and future goals remain secure.

It’s not about avoiding risk entirely — it’s about managing it intelligently.

- Key Components of Risk Management

Insurance Planning

Insurance Planning

- Life Insurance: Protects family against loss of income

- Health Insurance: Covers medical emergencies and hospitalization costs

- Critical Illness Insurance: Shields against major health events

Diversification

Spreading investments across asset classes — equity, debt, gold, and real estate — reduces exposure to market volatility.

Emergency Funds

A cash reserve covering 6–12 months of expenses prevents financial panic during unexpected events.

Estate and Legal Planning

Ensures assets are protected and distributed according to your wishes.

- Why Risk Management Matters

- Protects family from income loss due to untimely events

- Shields your portfolio from market and health risks

- Provides peace of mind, allowing you to focus on long-term wealth growth

- Ensures financial goals like children’s education, home purchase, and retirement stay on track

- Common Mistakes in Wealth Protection

- Relying solely on one type of insurance

- Neglecting emergency funds

- Overlooking diversification

- Ignoring inflation and rising healthcare costs

- Strategies for Effective Risk Management

1. Assess Your Risks

Identify potential threats to your income, health, and investments.

2. Choose Appropriate Insurance

Match coverage with your financial obligations and lifestyle needs.

3. Diversify Investments

Reduce portfolio risk by spreading across different assets and sectors.

4. Build an Emergency Fund

Keep liquid assets to handle unexpected expenses without selling investments at a loss.

5. Review Regularly

Life changes — so should your risk management plan. Review annually or after major life events.

- Dhingra Wealth’s Approach

We help clients create holistic wealth protection plans that include:

- Insurance planning for life, health, and critical illness

- Portfolio diversification strategies

- Emergency fund management

- Risk assessments aligned with financial goals

Our goal is to ensure wealth preservation while pursuing growth, so clients can invest with confidence.

- Key Takeaway

Building wealth is important, but protecting it is crucial.

A structured risk management plan ensures that financial setbacks do not compromise your long-term goals.

Partner with Dhingra Wealth to integrate risk management into your financial plan and secure your future.

Diversification — Reducing Investment Risk Through Smart Allocation

Investing is not just about chasing returns — it’s about managing risk while building wealth.

One of the most effective strategies to do this is diversification.

At Dhingra Wealth, we help clients create portfolios that balance growth and protection by spreading investments across asset classes, sectors, and geographies.

- What Is Diversification?

Diversification is the practice of investing in different types of assets to reduce exposure to any single risk.

The goal is simple: don’t put all your eggs in one basket.

By spreading investments, poor performance in one asset can be offset by stability or gains in others.

- Why Diversification Matters

- Reduces Risk: Minimizes the impact of market volatility on your portfolio

- Stabilizes Returns: Combines assets that perform differently under various market conditions

- Protects Against Uncertainty: Economic, political, or sector-specific events affect investments differently

- Supports Long-Term Goals: Helps achieve financial objectives without taking unnecessary risks

- How to Diversify Your Portfolio

Across Asset Classes

- Equity: Long-term growth potential

- Debt: Stability and predictable returns

- Gold: Hedge against inflation

- Real Estate: Tangible asset with appreciation potential

Within Asset Classes

- Equity: Mix of large-cap, mid-cap, and small-cap stocks or mutual funds

- Debt: Government bonds, corporate bonds, and fixed deposits

Across Geographies

Investing in domestic and international markets spreads geopolitical and currency risks.

- Common Diversification Mistakes

- Over-concentration in a single sector or stock

- Ignoring risk tolerance when allocating assets

- Failing to rebalance periodically

- Treating diversification as a one-time setup rather than an ongoing strategy

- Tips for Effective Diversification

1. Assess Your Risk Profile

Your age, income, and goals determine how much equity vs. debt you should hold.

2. Mix Growth and Safety

Combine high-risk, high-return investments with stable, low-risk assets.

3. Regular Portfolio Review

Market movements change asset weights — rebalance annually to maintain target allocation.

4. Avoid Herd Mentality

Diversify based on strategy, not trends or peer actions.

5. Seek Expert Guidance

Professional advice helps optimize diversification without overcomplicating your portfolio.

- Dhingra Wealth’s Approach

At Dhingra Wealth, we help clients:

- Build goal-based, diversified portfolios

- Optimize asset allocation for risk-adjusted returns

- Rebalance portfolios periodically to adapt to market conditions

- Educate clients on how diversification protects wealth

Our mission: maximize growth potential while minimizing unnecessary risk.

- Key Takeaway

Diversification is more than just spreading money across investments — it’s a strategic approach to managing risk.

A well-diversified portfolio keeps emotions in check, safeguards your wealth, and ensures smoother progress toward financial goals.

Critical Illness Insurance — Protecting Yourself and Your Family

Life is unpredictable, and medical emergencies can strike without warning.

While health insurance covers hospitalization, critical illness insurance goes a step further — providing a lump sum payout when diagnosed with a serious illness.

At Dhingra Wealth, we help clients protect their health and financial future with the right insurance strategies.

- What Is Critical Illness Insurance?

Critical illness insurance provides a fixed payout upon diagnosis of serious illnesses such as:

- Cancer

- Heart attack

- Stroke

- Kidney failure

- Major organ transplant

This payout is typically tax-free and can be used for medical treatment, lifestyle adjustments, or debt repayment.

- Why You Need Critical Illness Insurance

- High Medical Costs: Treatment for critical illnesses can drain savings quickly.

- Income Protection: Helps replace lost income if you’re unable to work.

- Family Security: Ensures your family’s financial stability during tough times.

- Supplemental Coverage: Complements your regular health insurance for comprehensive protection.

- Common Myths About Critical Illness Insurance

Myth 1: Health insurance is enough

Reality: Health insurance covers hospital bills but may not cover long-term expenses or loss of income.

Myth 2: Only older people need it

Reality: Critical illnesses can affect young adults too; early coverage is often cheaper.

Myth 3: It’s too expensive

Reality: Premiums vary by age, health, and sum insured — planning early makes it affordable.

- How to Choose the Right Plan

Assess Your Risk

Consider family history, lifestyle, and occupation.

Sum Insured

Choose a payout that covers treatment costs, recovery, and lifestyle maintenance.

Coverage of Illnesses

Check the list of covered illnesses and definitions carefully.

Premium Affordability

Balance between sufficient coverage and premiums you can pay comfortably.

- How Critical Illness Insurance Fits Into Financial Planning

At Dhingra Wealth, we view critical illness insurance as a pillar of wealth protection:

- Safeguards your financial plan against unexpected medical expenses

- Ensures your long-term goals like children’s education or retirement are not compromised

- Provides peace of mind, letting you focus on recovery, not finances

- Tips for Maximizing Coverage

- Buy policies early to benefit from lower premiums

- Combine with health insurance for comprehensive coverage

- Review policies periodically to ensure coverage keeps up with lifestyle and inflation

- Key Takeaway

Critical illnesses can disrupt life and finances, but planning ahead protects both.

With the right coverage, you can focus on recovery while ensuring your family’s financial security remains intact.

At Dhingra Wealth, we guide clients to select tailored insurance solutions that protect health, wealth, and peace of mind.

Managing Market Volatility — Strategies to Protect Your Portfolio

Market ups and downs are inevitable. While volatility can create opportunities, it can also trigger fear and impulsive decisions.

At Dhingra Wealth, we guide investors on how to manage market fluctuations without compromising long-term goals.

- Understanding Market Volatility

Market volatility refers to the rate at which stock prices or market indices rise and fall.

Factors driving volatility include:

- Economic data and corporate earnings

- Global geopolitical events

- Inflation, interest rates, and policy changes

- Investor sentiment and behavioral biases

Volatility is normal — even healthy — for markets, but emotional reactions can turn it into a financial risk.

- Why Investors Panic During Volatility

- Fear of Loss: Market drops trigger panic selling

- Herd Mentality: Following others leads to impulsive decisions

- Short-Term Focus: Ignoring long-term objectives in favor of immediate reactions

- Overconfidence or Greed: Chasing gains in uncertain conditions

- Strategies to Protect Your Portfolio

1. Diversify Investments

Spread investments across equity, debt, gold, and other assets to cushion market swings.

2. Focus on Long-Term Goals

Market dips are temporary; staying invested preserves the power of compounding.

3. Systematic Investment Plans (SIPs)

Investing regularly reduces timing risk and smooths out market volatility.

4. Maintain an Emergency Fund

Cash reserves prevent forced selling during market downturns.

5. Rebalance Portfolio Periodically

Adjust asset allocation to align with your risk profile and goals.

6. Avoid Emotional Decisions

Stick to your plan and avoid reacting to headlines or short-term movements.

- Role of a Financial Advisor

A professional like Dhingra Wealth helps:

- Assess your risk tolerance

- Build a balanced, diversified portfolio

- Provide perspective during market turbulence

- Ensure your investment strategy stays aligned with long-term goals

- Common Mistakes to Avoid

- Panic selling during temporary market drops

- Chasing hot stocks or sectors impulsively

- Ignoring asset allocation and risk diversification

- Neglecting review and rebalancing schedules

- Key Takeaway

Volatility is part of investing, but emotional investing amplifies risk.

By focusing on long-term goals, diversifying wisely, and maintaining discipline, investors can protect and grow their wealth even during turbulent markets.

Let Dhingra Wealth help you navigate market fluctuations with confidence and clarity.